Agentic Trading AI

Building adaptive trading systems with reinforcement learning and modular risk-managed architecture.

Why I Built It

Traditional trading bots rely on fixed rules.

I wanted to explore whether reinforcement learning could be used to build adaptive trading systems capable of learning decision‑making behaviour through experience rather than predefined rules.

This project became a research platform for studying agent behaviour, reward engineering, synthetic market generation, and risk‑aware trading execution.

System Architecture

The system separates signal generation, risk management, trade execution, and portfolio monitoring into modular components while reinforcement learning optimizes decision‑making behaviour.

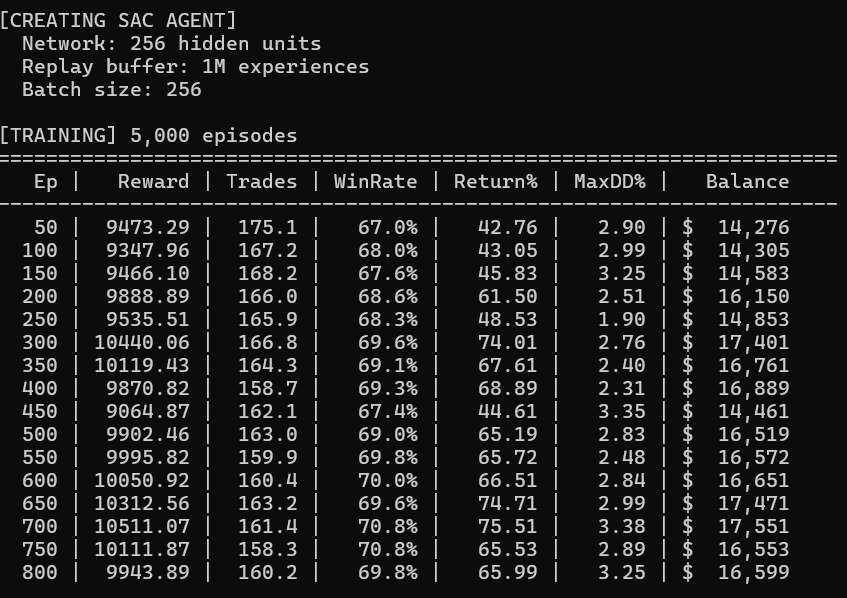

Training & Validation

Training run showing reward stability, trade frequency, win‑rate evolution, drawdown control, and account growth across thousands of episodes.

Technical Challenges

Reward Engineering

Designed reward functions that encouraged profitable behaviour while preventing the agent from avoiding trades entirely.

Policy Collapse

Resolved “never trade” failure modes through reward redesign and exploration tuning.

Synthetic Market Design

Built configurable market environments with trend and range regimes to create learnable training conditions.

Risk Management

Integrated dynamic position sizing, drawdown control, and trade lifecycle management into the training pipeline.

Results

Key Learnings

Building profitable AI systems is often more about environment design and reward engineering than model selection.

A large portion of the project focused on creating statistically valid training conditions and preventing agents from exploiting unintended reward structures.